Compensation for Risk

The bond market consists of various sub-asset classes, each reflecting different characteristics and types of risk. One key risk for investors is credit risk – the risk that an issuer may fail to meet its debt obligations, either by missing interest payments or being unable to repay principal. Credit spreads are one of the primary tools the market uses to quantify this risk, representing the additional yield an investor demands as compensation for taking on credit risk.

Creditworthiness

Creditworthiness is a measure of an issuer’s ability and willingness to repay its debt. Credit spreads are a key input in evaluating an issuer’s creditworthiness. They are calculated by subtracting the yield on a comparable-duration U.S. Treasury bond from the yield of the security in question. A higher spread signals greater perceived risk, while a lower spread reflects lower perceived risk.

Credit spreads fluctuate frequently to reflect new information about the issuer, as well as factors that may directly or indirectly affect its business. This includes developments in the issuer’s financial health, broader industry conditions, and macroeconomic trends. As credit risk increases, due to deteriorating fundamentals or external pressures, spreads widen to compensate investors for the added risk. Conversely, when credit conditions improve, spreads narrow.

The Cost of Uncertainty

Periods of surprise and uncertainty can catch investors off guard, leading to heightened volatility and reduced liquidity. A common mistake is failing to assign enough spread to account for these unexpected risks, especially when markets appear priced to perfection with tight spreads. When spreads are narrow, the margin for error shrinks, and new risks can cause spreads to widen quickly, leaving investors scrambling to react. This becomes problematic when investors have not sufficiently diversified or considered other investments where risk is more appropriately priced. In such environments, staying exposed to tight spreads, regardless of nominal yields, becomes harder to justify.

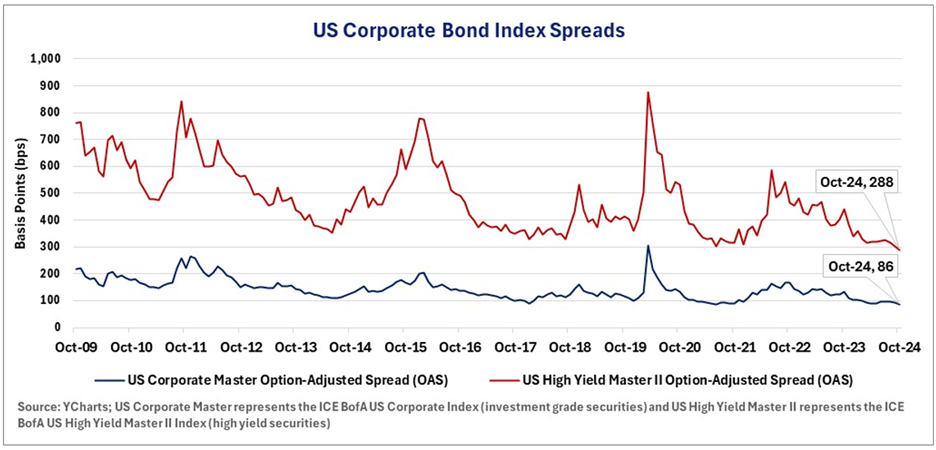

The chart below shows the month-end spreads of the investment grade (IG) and high yield (HY) corporate bond markets over the past 15 years. As we can see in the chart, the movements in spreads over time illustrate how market conditions and investor sentiment can shift dramatically.

Spreads of investment grade securities are relatively low when compared to high yield due to their historically low level of loss. In contrast, lower-quality securities, such as high yield corporate bonds, offer investors a liquidity premium in the form of structurally higher spreads, to compensate investors for their speculative nature. Regardless of credit quality, corporate credit spreads tend to widen sharply when new risks emerge, especially in high yield. This widening occurs because investors, having prioritized incremental returns, must reprice risk higher to account for new, significant information.

Valuations Matter

While the examples above focus on traditional corporate bonds, there are many other credit sectors where investors can assess spreads and other factors to identify relative value. Even when many sub-sectors are trading with tight spreads, additional analytics and tools can help differentiate between genuine opportunity and overpriced risk. Credit spread analysis is essential for evaluating credit risk and uncovering attractive opportunities.

Our approach to credit is grounded in the belief that investors should be compensated for the risks they take. We do not feel compelled to remain invested in an asset simply because it has demonstrated positive historical risk and return metrics. If an asset no longer offers adequate compensation and more attractive opportunities arise, we will realign our portfolios to focus on assets with compelling value. By focusing on valuations and staying mindful of unexpected risks, we aim to effectively manage both opportunities and risks for our clients.