Overview

Heightened volatility in August couldn’t derail stocks, and the S&P 500 closed the quarter at an all-time high. In the bond market, the three-month Treasury bill yield remained stable for much of the past year but began to decline ahead of the September Fed meeting, as expectations for a 50 bp rate cut grew stronger. Yields on the 3-month Treasury bill closed the quarter at 4.73%, while the 10-year Treasury fell to 3.81%.

As we move into the final quarter, investor sentiment is improving, bolstered by positive jobs data, cooling inflation expectations, and anticipated future rate cuts, which provide added confidence. The presidential election and earnings announcements will be key focal points for the market at the start of the fourth quarter, while the Fed continues to address inflation and shift its focus toward employment.

Topics of Interest

Market Valuations: The past twelve months have seen an unprecedented rise in valuations across most asset classes. Stocks, credit, gold, and U.S. Treasury bonds have posted strong returns relative to their historic averages. Traditional valuation metrics, such as P/E ratios for equities and corporate bond spreads in fixed income, currently appear expensive relative to long-term averages, offering less risk premium than investors might typically demand. While economic fundamentals may appear solid, our focus on valuations leads us to reposition for relative value.

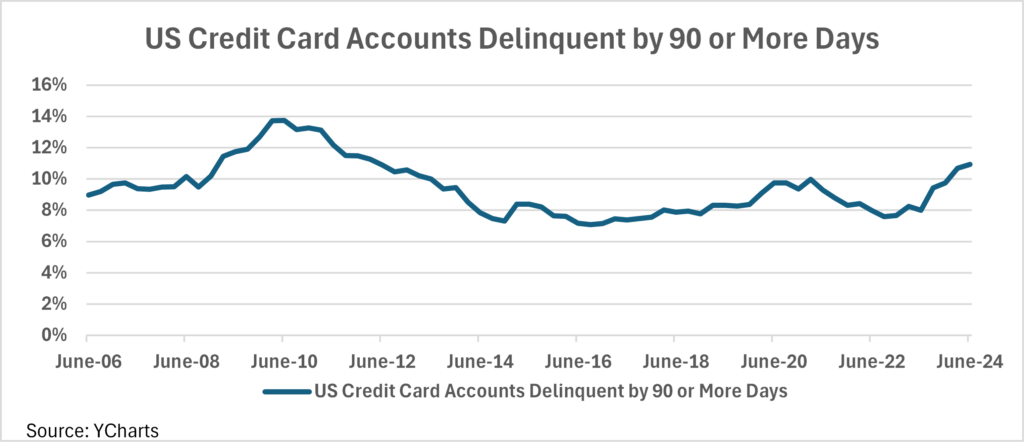

One area we are following is data about the US consumer. Amid rising consumer spending, concerns about sustainability are growing, particularly due to increasing levels of consumer debt. Although wages have risen to help consumers maintain some purchasing power lost from inflation, these higher input costs are likely to hurt employer profitability. Given that consumers represent a significant portion of U.S. GDP, markets should be wary of impacts to growth if employers lay off workers. Market data reveals that consumer housing debt and non-housing debt, notably from student loans, are increasing rapidly, along with rising delinquencies in credit card and auto loans.[i]

Consumer challenges present a potential headwind to the market’s positive outlook. If unemployment continues its slow, upward trajectory, the economy is likely to feel the impact of a slowing consumer. While increased government spending could partially offset this slowdown, risks to consumer cyclical sectors remain. Furthermore, such spending also reintroduces the risk of rising inflationary pressures, posing a more serious challenge for the Federal Reserve – stagflation.

Stagflation: The topic has emerged in discussions among few analysts in the media, yet such an outcome is possible. Massive stimulus in recent years has helped offset the impact of higher costs on the economy, and markets should not expect this level of support to continue. A slowdown in government spending, coupled with tight monetary conditions and a slowing consumer, could adversely affect employment and growth, while loosening conditions to provide relief could reignite inflation.

The years of zero interest rate policy appear to be behind us, and markets are still adjusting to higher costs of capital. Fiscal stimulus and bailouts have masked some of the risks traditionally associated with higher interest rates. Sluggish or stagnant economic growth, combined with supply-side risks and elevated interest rates, presents stagflation as a genuine risk to the economy.

Strategy

As we assess our thoughts about US consumers and valuations, we aim to lower overall risk in our asset allocation. Our primary focus is to mitigate drawdown risk while recalibrating our exposures to emphasize income-generating assets. We view income as a cushion against volatility and look to credit markets to enhance our risk-adjusted return profile.

In the credit space, various liquid options are available to provide diversified exposure to segments of the market that offer adequate compensation. We continue to prefer structured credit, particularly CLOs, while also recognizing value in mortgage credit and asset-backed sectors. These assets offer attractive yields with total return potential, and less sensitivity to interest rates than traditional bonds.

In rate markets, Treasury yields appear to be pricing in more cuts than are likely to occur outside of an economic downturn, limiting their total return potential. We are ready to add to our duration position as rate volatility returns. In the meantime, we prefer to generate returns from credit. Elsewhere in high- quality bonds, investment-grade corporate and municipal bond valuations are generally less attractive than other segments of the credit markets.

Finally, liquidity is crucial for our portfolios, especially in credit, where a trend has been emerging among investors seeking illiquid or semi-liquid solutions to mitigate volatility. Fortunately, we can source similar return opportunities for our clients in liquid markets. Both volatility and illiquidity come with a cost, and we see significant advantages to favoring liquidity in today’s environment. The current price for liquidity differs from its true cost when demand surges. Investors pursuing less-liquid exposures because of potential volatility benefits should reassess their liquidity needs, and the premium required.

Outlook

As we head into the home stretch of 2024, our focus is primarily on valuations. The market’s already lofty valuations may continue to climb, fueled by emotions and the fear of missing out, as often occurs after periods of strong returns. Consequently, investors may underappreciate looming risks that may not be evident in the current and lagging economic data. We anticipate an upward trend in unemployment and recognize that inflation may remain stubborn for longer, although we do expect its rate of change to continue to decline as long as the Fed doesn’t adjust policy too dramatically.

Despite our concerns, we see plenty of opportunities in credit markets for income and total return. Given that equities are the primary driver of portfolio risk and are closely tied to economic conditions, we are reducing equities in favor of credit. This shift allows us to mitigate potential drawdowns while improving risk-adjusted returns for our client.