Adapting to the Market

Bonds have historically served as a key component in portfolios, offering investors a steady stream of income and diversification benefits. However, the bond market contains a variety of sub asset classes, each with distinct risk profiles and characteristics. The risks associated with these markets can vary significantly and evolve over time. As a result, diversification strategies that were once considered beneficial may no longer be suitable. Investors must adapt to ensure their strategies align with current risk objectives.

Key Risks for Investors

Bond investors primarily encounter two key risks: interest rate risk and credit risk. Interest rate risk affects securities sensitive to interest rate changes, such as investment grade bonds, which typically have long durations and lower default rates than their high yield counterparts. Credit risk is more relevant for sub-investment grade securities rated BB or below, as these experience higher default rates and face increased scrutiny regarding creditworthiness. It is important to note that bonds can possess both risks, and their typical risk profiles can shift depending on the market’s assessment of current conditions.

Traditional Exposures

Independent investors have traditionally sought high quality fixed income securities to generate income as these are perceived to be safer and likely to offer lower principal risk. These include tax-exempt municipal bonds and taxable investments in US treasuries, agencies, and investment grade corporate bonds, often with shorter durations.

Yet, solely investing in traditional taxable securities can lead to overexposure to interest rate risk. Despite varied exposure to sectors and quality, these assets are highly sensitive to interest rate changes and thus strongly correlated. While the portfolio appears diversified categorically, it remains vulnerable to interest rate risk. In a traditional bond portfolio, interest rate risk – as measured by duration – is the key risk driver.

In contrast, assets such as high yield bonds and senior loans are less sensitive to interest rates, though they carry greater credit risk. Floating-rate loans and collateralized loan obligations (CLOs) carry minimal direct interest rate risk and offer higher yields to compensate investors for the additional credit and liquidity risk associated with high yield securities.

Benefits of Credit

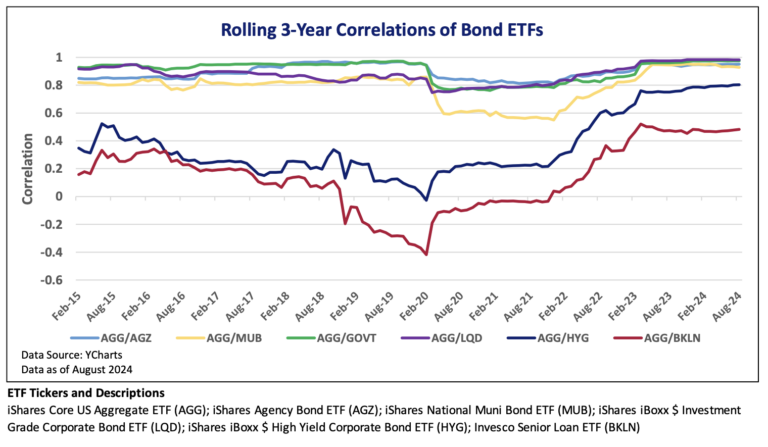

The following chart illustrates the rolling three-year correlations of various passive fixed income ETFs, highlighting some key insights. High quality, interest rate sensitive markets, represented by passive ETFs like AGG, AGZ, MUB, and LQD, show a strong correlation with one another over time. This suggests that these asset types tend to move in tandem, especially with changes in interest rates.

Conversely, credit assets such as HYG and BKLN display lower correlations with these interest rate sensitive bonds. This indicates that high yield bonds and banks loans can behave differently under varying market conditions. As a result, incorporating these credit assets into a traditional bond portfolio may enhance diversification, helping to reduce overall portfolio risk and potentially improve returns.

Understanding correlation is essential for portfolio management. It measures how two variables move in relation to each other. Assets with a correlation above zero are positively correlated while those below zero are negatively correlated. Correlations closer to +1 or -1 indicate stronger relationships. A correlation above 0.70 is considered strong. While passive ETFs can demonstrate the risk and return of an asset class, actively managed strategies can introduce variability not captured in this analysis.

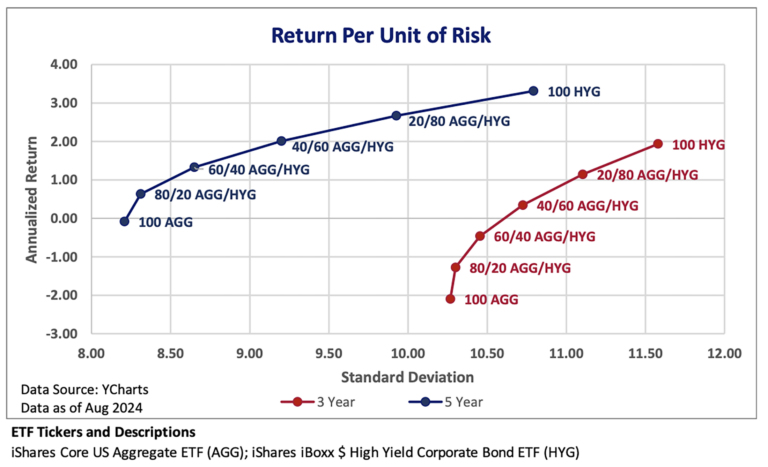

The next chart shows that adding high yield bonds (HYG) could have enhanced portfolio efficiency over the past three- and five-years ending August 2024. While HYG is more volatile than AGG, adding 20% to a core bond allocation could have improved returns with minimal additional risk. The addition of high yield also boosts the overall yield of the portfolio, resulting in greater income distribution to investors.

Active Management

Bond investors can enhance traditional interest rate-sensitive portfolios by integrating credit and maintaining a strong awareness of risk. As asset classes evolve and new risks emerge, correlations may shift over time. Since there is no guarantee that past correlations will remain effective indefinitely, understanding the drivers of risk in a portfolio and their relationships is critical for any investor aiming to diversify risk and improve returns. To address changing risks, we actively manage our client portfolios, leveraging our expertise to navigate forward-looking challenges and identify opportunities that adequately compensate us for those risks.