Overview

The recent economic environment has been positive while markets have remained resilient. On the back of AI, favorable earnings, and expectations of multiple rate cuts to start the year, risk assets have delivered strong returns year-to-date. Interest rates have remained unchanged despite expectations for several cuts at the start of the year and though treasury yields have trended lower. The rate of inflation has declined although forecasts for rate cuts continue to be pushed back as the Fed waits for more convincing data. The market is currently expecting the Fed to cut interest rates by 25bps in September.

Further supporting stocks in 2024 is another strong year of stocks buybacks. Goldman expects S&P 500 companies to buy back over $900 billion of stock in 2024 and a record of over $1 trillion in 2025. As a reminder, buybacks reduce the number of shares outstanding and all else equal, increasing a company’s earnings per share. Earnings per share (EPS) is the key metric used by the Street to evaluate stocks.

Topics of Interest

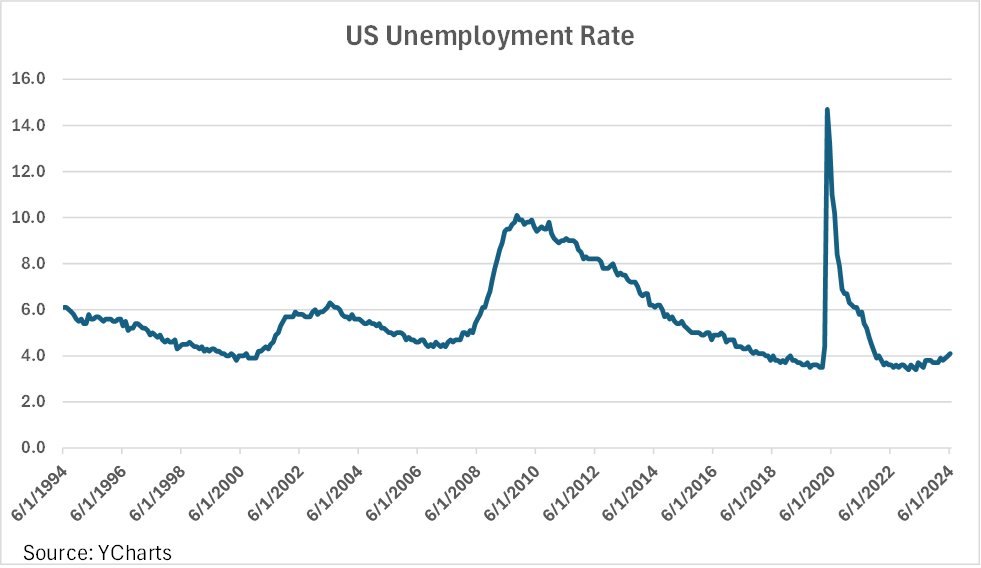

Unemployment: Since the lows of 3.4% were achieved in the Spring of 2023, the unemployment rate has been trending higher and recently breached 4%. We see continued challenges to economic growth that will lead to firms cutting back staff. As such, the U-3 unemployment rate will continue its rise as firms grapple with the higher cost of capital and the end of fiscal support, which will lead to a slowdown in growth.

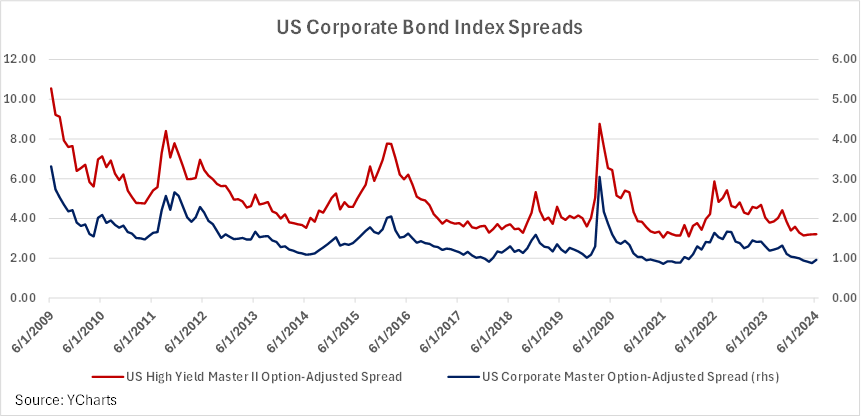

Corporate Credit Valuations: Overall, bonds are offering terrific value with relatively high nominal yields for income focused investors. However, corporate credit spreads are relatively tight when compared to historical averages, especially when we adjust for many near-term risks. Spreads are a measure of the additional yield investors demand above a treasury security of similar maturity to compensate them for the potential loss given default.

We like treasuries at current levels though we expect better buying opportunities across the broader credit markets in the months ahead. While nominal yields provide investors with strong cash flows not seen in over a decade, the chart below demonstrates that investors are accepting lower yields for credit risk. We expect defaults to rise in the next 12-18 months and as a result, spreads to widen. We are cautious as valuations do not reflect our forward-looking risks.

Mortgage Credit: Residential property has performed well while segments of the commercial markets remain challenged. Market valuations, especially in commercial sectors, have begun to reflect some of the near- term risks and yields in mortgage credit are garnering attention. Long-term value is being created; however, the persistently high level of interest rates among other factors will continue to exert pressure on areas of the commercial sector. Furthermore, a recession will create additional challenges.

Strategy

We are cautious heading into the second half of the year, using treasury duration to hedge some credit risk while also holding cash as dry powder for better entry points. Investor demand for treasuries should be expected to increase as volatility returns, which should support our duration position. We are highly liquid and continue to look for relative value opportunities across all segments of credit. In the meantime, we are focused on generating high cash flows with a credit barbell approach.

Our view on risk and reward in corporate credit is unfavorable. While credit markets are fundamentally healthy, investment grade and high yield corporate spreads are simply not attractive. We prefer structured and securitized credit opportunities as alternative sources of yield where investors are better compensated for the risks.

Mortgage credit has experienced strong performance with the market’s anticipation of interest rate cuts. Unfortunately, the aggressive rate cut expectations have not occurred and lenders are feeling the impact from higher interest rates. They are likely to experience an increase in loan losses and delinquencies, which could lead to dividend cuts and sharp price declines. Ultimately, this will create more attractive valuations for investors to purchase securities at steep discounts. Until then, we remain patient and selective in securities with attractive long-term prospects.

Municipal bonds might be somewhat compelling to investors in the highest tax brackets, but overall valuations are not enticing. Muni/treasury ratios have improved over the quarter, yet spreads remain tight as positive technicals (strong investor demand coupled with low new issue supply) continue to support the market. We see better opportunities to generate strong after-tax income and total return in the taxable market. Munis would become more interesting if both ratios and spreads gapped higher.

Outlook

The several rate cuts expected throughout 2024 have not materialized, yet equities continue to surge to record highs. Going into the second half of the year, US Presidential elections, stubborn inflation, fading fiscal support, and the lag effect on the economy from higher interest rates should pressure risk assets, especially stocks. We expect unemployment to rise looking ahead and a recession to follow, which should lead to defaults. Credit appears to be a better risk adjusted asset relative to equities over the near term and we will rely on income as a key driver of return in the quarters ahead.