For decades, the U.S. dollar has been the cornerstone of global finance, supporting international markets and investments. But that dominance is no longer assured. As technologies and global systems evolve, digital currencies gain traction, and the global landscape shifts, the dollar’s influence is being redefined. This transition is already underway, prompting investors to pay closer attention to how the dollar’s role may be shifting within a changing global system.

Reserve Currency Under Pressure

Since World War II, the U.S. dollar has been the dominant global reserve currency. However, its share of global foreign exchange reserves has declined from 65% a decade ago to roughly 58% today.¹ While it remains the primary reserve asset, many economies are increasingly diversifying their holdings.

The Chinese yuan is gradually gaining ground, supported by cross-border payments, central bank swap agreements, and growing use of the digital yuan in international trade.² Europe is also exploring alternatives; European Central Bank President Christine Lagarde has highlighted the euro’s potential for a stronger global role amid broader economic shifts.³

The dollar’s resilience has long been underpinned by a stable U.S. economy, favorable interest rate differentials, and the depth of the Treasury market. These factors have sustained demand even during times of market stress. But as monetary systems evolve and concerns over U.S. debt grow, the dollar’s long-standing dominance is facing renewed scrutiny.

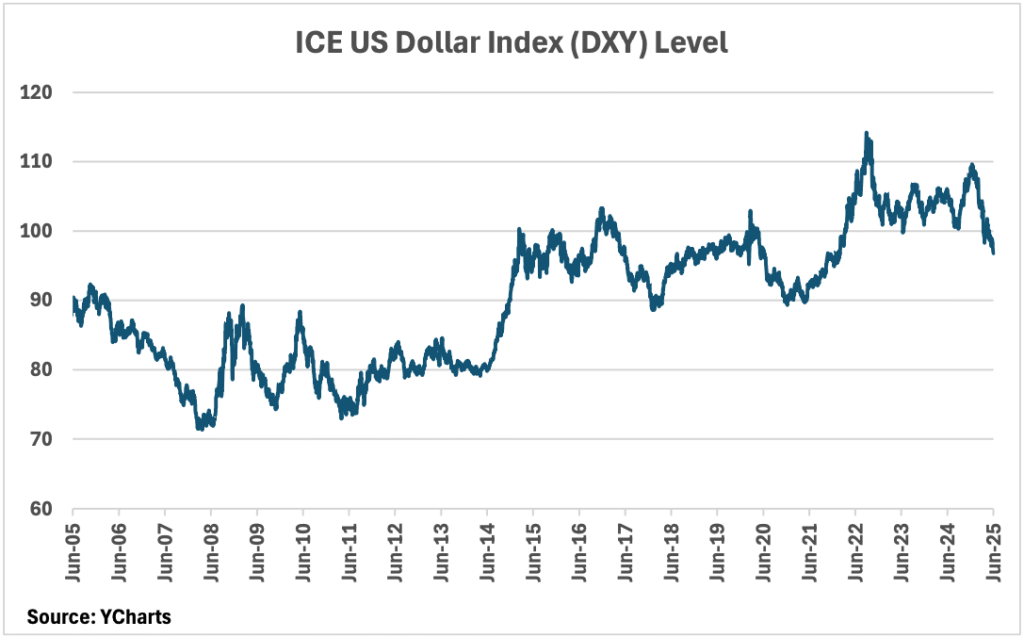

Policy Uncertainty and Market Response

As U.S. economic policy becomes less predictable, market anxiety is rising. In the first half of 2025, the U.S. Dollar Index (DXY) fell by roughly 10 percent, its steepest first-half drop since 1973.⁴ Recent CFTC data shows speculative net short positions in the dollar at their deepest in two years, while global fund managers are holding their largest underweight in the greenback in two decades.⁵ These shifts reflect growing investor concern over fiscal direction, trade friction, and the Fed’s policy path.

Still, institutional trust in the dollar hasn’t vanished. HSBC’s CEO reaffirmed the dollar’s unmatched global infrastructure and reliability earlier this year,⁶ a reminder that no immediate rival matches its scale, even amid headwinds. Nonetheless, global policymakers are preparing for a more diversified system. Many regions worldwide are implementing new payment and currency frameworks such as regional networks and digital currencies to modernize cross-border transactions, improve financial resilience, and contribute to a more competitive international monetary landscape.⁷

Capital Flows and Global Impact

Cross-border capital flows impact financial market growth, cost of capital, and currency values, and these factors, in turn, influence capital movements. Changes in the value of the dollar and uncertainty about U.S. fiscal policy can alter the pace and direction of international capital, impacting global markets. This creates complexity for investors navigating a shifting landscape. While capital has long flowed into the U.S., growing policy uncertainty may drive diversification into other markets and assets.

Portfolio Implications and Looking Ahead

The dollar remains a pillar of global finance, but its dominant position should not be taken for granted. Structural shifts in the international monetary system and evolving macroeconomic forces are gradually challenging long held assumptions. While the dollar is not disappearing, the system around it is becoming more diverse, creating new risks and potential openings for those who are paying attention.

Is the dollar technically oversold right now? Possibly. But markets are always in motion, and assuming its strength will endure untested overlooks deeper trends. Investors should stay alert, assess the landscape with fresh perspective, and remain flexible in how they position their portfolios. In an environment that is constantly changing, awareness and adaptability are not just advantages, they are necessities.

Sources

¹Federal Reserve – “The International Role of the U.S. Dollar: Post-COVID Edition,” June 2023 – https://www.federalreserve.gov/econres/notes/feds-notes/the-international-role-of-the-us-dollar-post-covid-edition-accessible-20230623.htm

²Reuters, April 29, 2025 – “China ramps up global yuan push, seizing retreating dollar” – https://www.reuters.com/world/china/china-ramps-up-global-yuan-push-seizing-retreating-dollar-2025-04-29/

³Reuters, July 2, 2025 – “Joint European defence borrowing could bolster euro’s global role, ECB’s Rehn says” – https://www.reuters.com/business/finance/joint-european-defence-borrowing-could-bolster-euros-global-role-ecbs-rehn-says-2025-07-02/

⁴MarketWatch – ICE U.S. Dollar Index (DXY) – https://www.marketwatch.com/investing/index/dxy

⁵Reuters, June 18, 2025 – “Dollar exit could be crowded” – https://www.reuters.com/markets/currencies/dollar-exit-could-be-crowded-some-time-2025-06-18

⁶Financial Times, April 2025 – “HSBC chief says dollar still unrivaled despite geopolitical shifts,” https://www.ft.com/content/027b9402-e2e5-41a2-9e9b-6d9489e65126

⁷IMF, June 18, 2024 – “Central Bank Digital Currencies Can Boost Middle East’s Financial Inclusion and Payment Efficiency,” https://www.imf.org/en/Blogs/Articles/2024/06/18/central-bank-digital-currencies-can-boost-middle-easts-financial-inclusion-payment-efficiency